Both the total number of SR&ED claims filed over the past year and the investment tax credits (ITCs) dispersed made a noticeable year-over-year jump, according to the latest statistics from the CRA.

A total of 21,525 SR&ED claims were filed and 21,537 were processed from April 1, 2023 through March 30, 2024, with $4.4 billion dollars claimed and $4.2 billion allowed (or dispersed) during the period.

This marks an increase from 20,464 claims filed during the 2022-2023 window and 20,332 claims filed during the same period over 2021-2022.

The growth in total ITCs claimed was even more stark: Compared to the $4.4 billion in the most recent fiscal year, only $3.4 billion were claimed as of March 2022 and $3.8 billion by March 2023.

At the same time, however, the percentage of claims accepted as filed within 60 days of delivery has dropped for the third consecutive year: Only roughly 92 percent of claims “accepted as filed” during this window in 2023/2024, which is a steady decline in Service Standards from 94 percent the previous year and 98 percent the year before that.

What does this mean for SR&ED claimants?

On the one hand, despite there being no lag in the generosity of the government’s banner research and development tax credit, the Canadian Revenue Agency is taking more time to evaluate and qualify claims.

This is evidenced by the drop in claims accepted outright within 60 days, which on the one hand is indicative of the CRA simply working with a larger workload.

But there’s also good reason to believe that with the federal government tightening its coffers in response to budgetary constraints (see our recent Budget 2024 coverage to learn more), the CRA is taking extra scrutiny in evaluating every claim filed before dispersing non-dilutive funding. The logic here is that “every dollar counts” and the government wants to ensure any investments they endorse for innovation will be well placed.

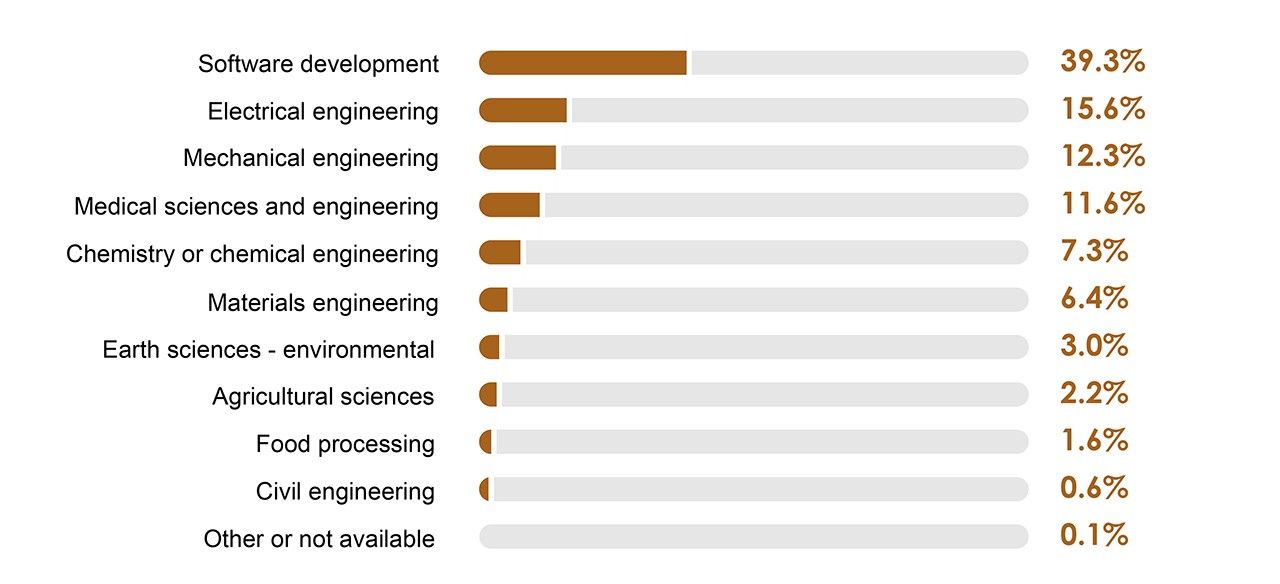

More funding for Software development in 2024

As for the industries that benefit most from SR&ED funding, Software development remained the primary benefactor for at least the third consecutive year. More than 39 percent of ITCs were dispersed to this sector through SR&ED over the last year, which has grown from a relatively static 34.9 percent and 35.7 percent during the two previous April-March windows.

Electrical engineering and Mechanical engineering were the runners up again for the 2024 period, enjoying roughly 16 percent and 12 percent of ITCs between 2023-2024.

Source: Canadian Revenue Agency Scientific Research and Experimental Development (SR&ED) tax incentives Annual program statistics.

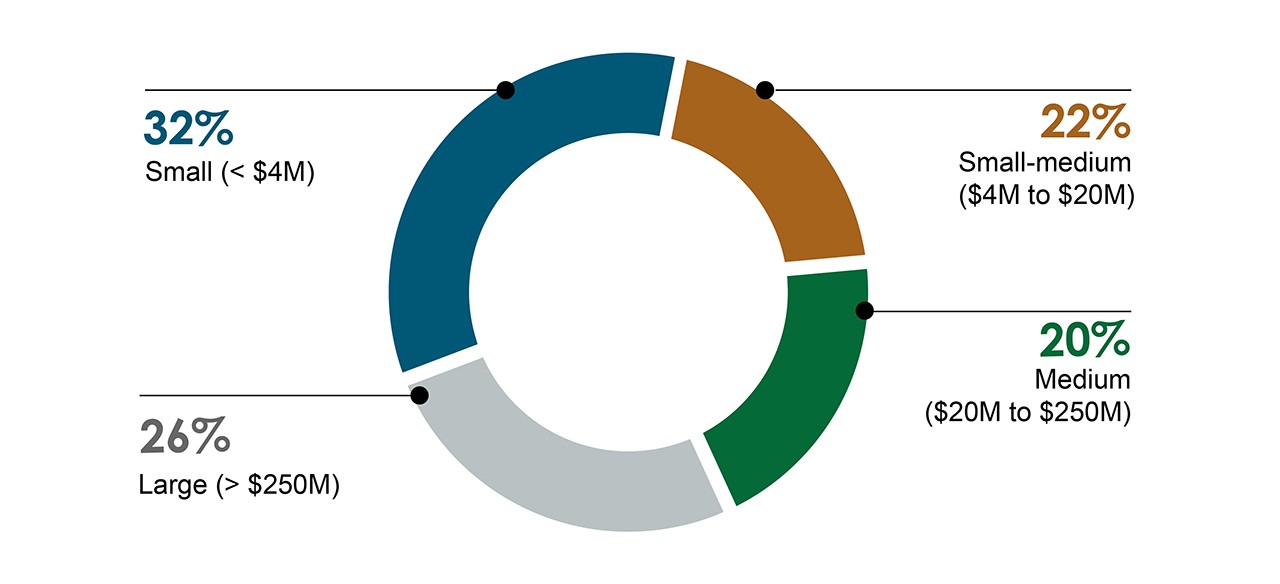

The breakdown of business size remained relatively static year-over-year as well, with 32 percent of SR&ED funds going to small businesses (which the CRA classified as businesses with less than $4 million in gross income).

Small-to-medium businesses ($4-$20 million in gross income) received 23 percent, Medium businesses ($20-250 million in gross income) received 20 percent and Large businesses with greater than $250 million taking home just 26 percent—despite large businesses accounting for just 3 percent of claims filed.

Source: Canadian Revenue Agency Scientific Research and Experimental Development (SR&ED) tax incentives Annual program statistics.

With greater CRA scrutiny, claim quality is critical

Despite continuing to dole out significant innovation funding via the SR&ED program, the CRA is now clearly taking a closer look at every claim filed, which is resulting in payout delays regardless of whether teams qualify.

This puts the onus on filers to be diligent in the quality, accuracy and completeness of their SR&ED claims to minimize their risk of delays—especially if they depend on SR&ED funding as a key component of their capital strategy.

At the same time, it’s likely that SR&ED audits will go up this year as well to align with the “every dollar counts” logic related to the delays in accepted claims. While the data here is largely anecdotal, it’s more important than ever that teams are prepared to defend their claims should the CRA target them for an audit.

At Boast, we not only streamline the claim process to deliver comprehensive, detailed and defensible claims, we also do the heavy lifting for you when it comes to making your case to the CRA.

Without a knowledgeable partner like Boast that has unmatched technical and tax expertise to navigate the thorny process of SR&ED audits, your team could get derailed and waste many hours trying to get your claim through to approval.

Talk to one of our SR&ED experts today to ensure your claim is filed with minimal incident and our Auditshield guarantee.

SR&ED 2024 program statistics FAQ

- What are the latest SR&ED claims statistics for 2023/2024? There was an increase in both the total number of SR&ED claims filed (21,525) and investment tax credits dispersed ($4.4 billion) from April 2023 to March 2024, compared to previous years. However, the percentage of claims accepted within 60 days dropped to 92%.

- What do the changes in SR&ED claims processing mean for claimants? The CRA is likely scrutinizing claims more closely due to budgetary constraints, leading to longer processing times. Claim quality and defensibility are now critical to minimize delays and audits.

- Which industry benefited the most from SR&ED funding in 2024? Software development remained the top beneficiary, receiving over 39% of the total investment tax credits dispersed through the SR&ED program from 2023 to 2024.</Answer>

- How was SR&ED funding distributed among businesses of different sizes? Small businesses (under $4M gross income) received 32% of SR&ED funds, small-to-medium businesses ($4M-$20M) got 23%, medium businesses ($20M-$250M) received 20%, and large businesses (over $250M) received 26% despite accounting for only 3% of claims.

- What is the recommendation for filing successful SR&ED claims? To minimize delays and audits, it’s recommended to work with knowledgeable partners like Boast who can ensure comprehensive, accurate, and defensible SR&ED claims while providing expertise in navigating the audit process.